Key takeaway: Identity theft insurance won’t usually cover the direct financial losses that result from fraud, only expenses related to recovering your identity.

Call us:

1-800-416-0599

Identity theft insurance: What is it and is it worth it?

You probably already insure your vehicle, home, and health. Should you add your identity to the list? Keep reading to learn more about identity theft insurance, what it covers, and whether it makes sense for you to get it.

There’s a victim of identity theft every five seconds in the U.S. — and you don’t need to do anything unusual to be at risk. Your sensitive information could be exposed through everyday activities like online shopping, banking, and browsing. While no product can guarantee that your identity will never be stolen, identity theft insurance can provide financial assistance if it is.

What is identity theft insurance?

Identity theft insurance is a type of insurance that helps cover some of the costs that may arise if your identity is stolen. It doesn’t prevent identity theft, but it can mitigate its financial consequences, as restoring your identity can be an expensive and time-consuming process. Complex identity theft cases can sometimes even require legal assistance.

Policies usually cover costs associated with restoring your identity and recovering from the incident. However, financial losses incurred before the identity theft was detected — like stolen funds, fraudulent purchases, or debts from accounts opened in your name — may not be covered. Always review specific policy details carefully to understand what’s included and what isn’t.

How does identity theft insurance work?

Identity theft insurance works similarly to home or auto insurance, offering financial assistance if your identity is compromised. But it may not cover all costs immediately. Depending on your policy, you might need to pay certain expenses out of pocket during the recovery process. As long as those expenses qualify, your insurance provider should reimburse you up to the limits outlined in your plan.

How and what you can claim will depend on the type of identity theft and your policy’s terms and conditions. Depending on what personally identifiable information (PII) an ID thief has, the consequences could range from a damaged credit score to lost employment opportunities if you don’t act quickly to recover your identity.

What does identity theft insurance cover?

Identity theft insurance policies typically cover some of the expenses incurred during the identity theft credit repair process. However, they’re less likely to cover direct financial losses that occur immediately after the theft, such as stolen funds from your bank account or fraudulent charges on your credit card.

Here’s a list of expenses that might be covered, depending on the specific policy:

- Bank fees charged in connection with fraudulent activity on your account.

- Notary fees for obtaining certified copies of your identity documents.

- Lost wages if you need to take time off work for activities to restore your identity (for example, to meet with your attorney).

- Legal fees if you need to hire an attorney for consultations or to represent you at court hearings.

- Credit agency fees for placing fraud alerts on your credit reports and obtaining copies of your credit reports.

- New document costs for replacing important identifying documents, like a stolen or lost Social Security card or driver’s license.

- Specialist fees for identity restoration consultants who can work with your creditors, credit bureaus, credit card companies, and other financial institutions to help guide you through the identity recovery process.

- Long-distance phone bills relating to your identity theft restoration.

- Postage costs for registered mail and expedited shipping of documents.

- Child care costs if you need to pay for child care while taking steps to restore your identity.

- Other financial fees, such as loan reapplication fees if you’re denied credit due to fraud from identity theft.

Is identity theft insurance worth it? Three questions to ask yourself

Reclaiming your identity can be slow and costly. Having insurance can ease that burden, but whether it’s worth it depends on your risk tolerance and how much hassle you’re willing to endure if, like 75 million other Americans,* you fall victim to identity theft.

Of course, you’ll also want to weigh up the benefits against the cost of an identity theft insurance policy. Prices vary based on coverage and provider, and out-of-pocket deductibles may apply. It’s also worth checking whether your existing insurance policies already include identity theft protection.

1. Do I have existing protection?

You may already have some form of identity theft protection insurance through your credit card company, employer, or your home or renters insurance policy. In 2020, the Insurance Information Institute reported that “Few U.S. homeowners and renters realize their existing insurance policies offer them limited identity (ID) theft coverage.”

So it pays to check if you already have some form of identity theft insurance or protection services. Just make sure the coverage meets your specific needs and provides the level of protection that’s right for your situation.

2. Can I take care of it myself?

Resolving identity theft problems and recovering your financial identity can take time and cause stress. Ask yourself how willing you are to navigate bureaucracy, read through small print, and spend time on the phone if your identity is stolen.

Also, remember that identity theft insurance isn’t the same as identity theft protection. Insurance usually only helps after you’ve already become a victim. By contrast, protection services can alert you to warning signs early, saving you time and money later.

Here are some steps you can take to help protect your identity:

- Freeze your credit. This is a particularly good option if you’re not actively applying for credit.

- Monitor your credit reports regularly.

- Check your bank and credit card accounts regularly, looking for suspicious transactions or withdrawals.

- Learn how you can protect yourself against identity theft and follow our tips on ways to avoid it.

- Use a dedicated identity theft protection service such as LifeLock Standard. LifeLock will notify† you of suspicious and potentially fraudulent use of your personal information, helping protect you against identity fraud and restore your identity if you ever fall victim.

3. How much am I at risk?

Another consideration when deciding whether to sign up for identity theft insurance is how at-risk you think you are. Your behavior and how you protect your personal information online can increase or mitigate your risk of becoming an identity theft victim.

Ask yourself these questions:

- Do I use strong passwords?

- Do I use two-factor authentication to log into my accounts?

- Do I safeguard my personally identifiable information?

- Do I know where all my important documents are?

If you answered yes to these questions, then you’re already taking steps to mitigate your risk of identity theft.

Although there are laws that cap losses for fraudulent transactions on bank accounts and credit cards, you’re still at risk of damaging your credit score if identity thieves take out loans, credit cards, utility accounts, or other lines of credit in your name.

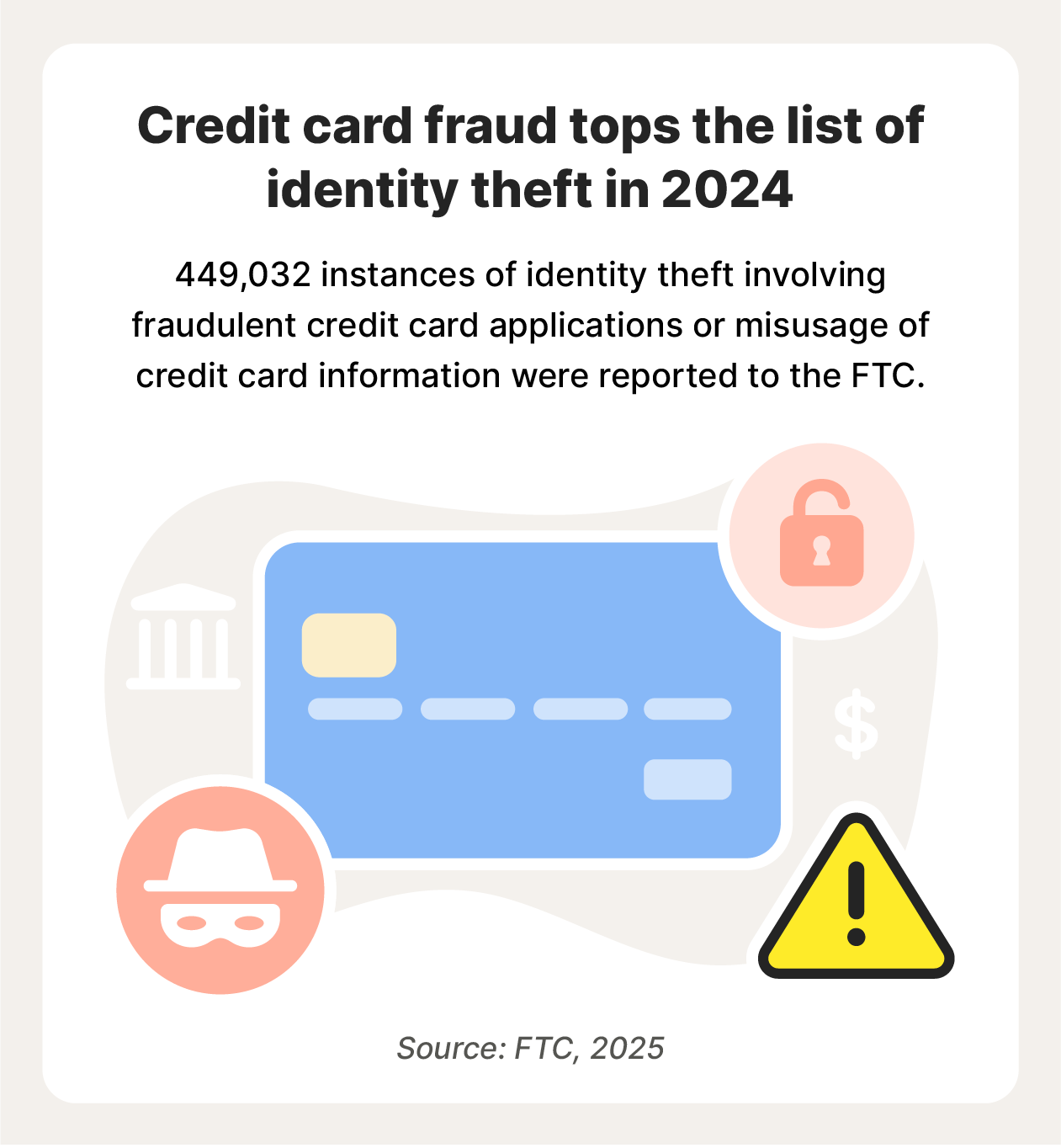

According to the FTC (Federal Trade Commission), more than one million Americans reported identity theft in 2024, with credit card fraud being the most reported type of identity theft. Given these numbers, it’s not surprising that many customers have decided identity theft protection is worth it to help monitor their accounts and possibly catch signs of identity theft early.

449,032 instances of credit card fraud were reported to the FTC in 2024.

Where can you get identity theft insurance and protection?

If you’re looking to get identity theft insurance or want to sign up for an identity theft protection service, make sure you know what is included. Most identity fraud insurance policies are designed to help reimburse you if you become a victim, whereas identity theft protection services aim to help alert you to signs of identity theft and remedy its consequences.

When choosing an identity theft insurance policy, consider factors like coverage limits, additional services offered, and the insurance provider’s reputation.

If you’re looking for protective measures to supplement your identity theft insurance policy, then a LifeLock Standard membership is a good place to start. In addition to extensive personal data and credit monitoring, our dedicated restoration specialists will help you fix issues if your identity is stolen.

Insurance providers

Most insurance providers offer identity theft insurance. If you already have other insurance policies, such as home, renters, or car insurance, you may be able to get identity theft insurance as an add-on to your existing policy. It may even already be included. Alternatively, you could buy insurance for identity theft from a different provider, allowing you to shop around for the best deal.

Credit card companies

Some credit card providers offer identity theft insurance or protection services automatically or as an add-on. Check with your credit card provider to find out what they offer and what may already be included with your current credit card.

Identity theft protection services

Identity theft protection services differ from identity theft insurance. These services typically include expert support to help resolve issues if your identity is stolen, along with ongoing monitoring to detect unauthorized use of your personal information, so you can respond quickly if identity theft occurs.

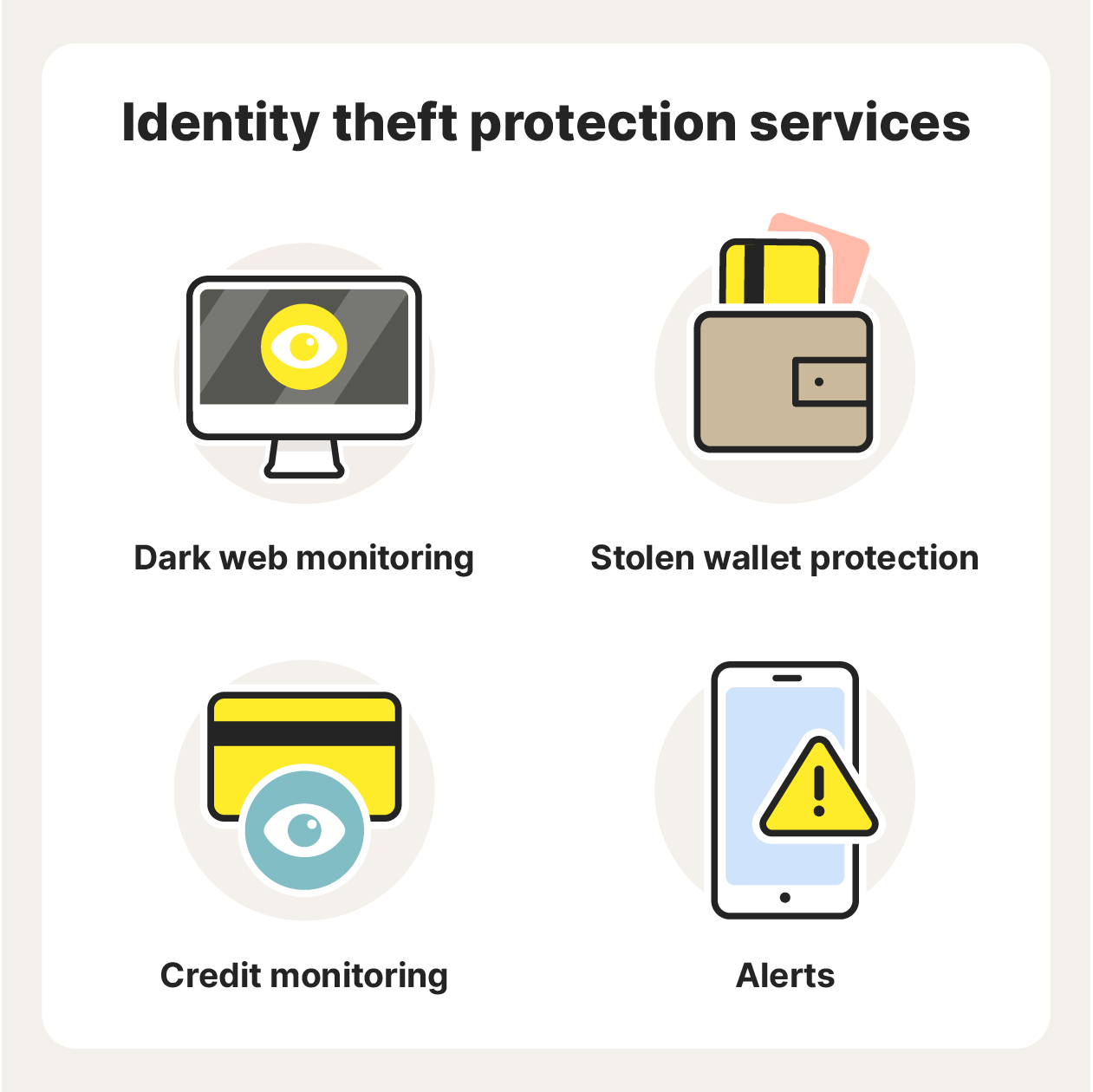

Identity theft protection services usually include features such as:

- Dark web monitoring§ that scours the dark net for traces of your personal information being sold or traded by criminals, so you can secure your accounts after a data breach or leak.

- Stolen wallet protection that assists with canceling cards and organizing replacements.

- Credit monitoring that keeps an eye on your credit score with credit agencies to detect fraud.

- Alerts† that notify you when your personal data is used in applications for loans and credit cards.

Make sure you know what is and isn’t included in the offer you’re considering to help you decide which plan is right for you.

Identity theft protection can help monitor your identity.

How much does identity theft insurance cost?

Identity theft insurance generally costs between $20 and $60 a year. However, the price depends on a few factors, including where you live and how comprehensive the coverage is. But it’s not just the policy cost to take into consideration — you should also ask the following questions:

- What are the policy limits?

- Is there a deductible?

- If lost wages are covered, what triggers this coverage?

- If a policy covers legal fees, does legal work need to be pre-approved by the insurer?

Choose the best option for your situation

Identity theft is a growing threat that demands proactive, multi-layered defenses to help keep your personal information safe.

If you become a victim, having identity theft insurance offers strong benefits. As a supplement, consider using an identity theft protection service, too. Look for a comprehensive protection service that includes privacy monitoring, stolen wallet protection, credit monitoring, and help recovering your identity should you fall victim.

FAQs

What doesn’t identity theft insurance cover?

Identity theft insurance typically doesn’t cover financial losses incurred before the theft is detected, such as stolen funds, fraudulent purchases, or debts from credit lines opened in your name. Instead, policies are generally designed to help cover some of the expenses involved in restoring your identity.

Can you get free identity theft protection?

You may have access to free identity theft protection through your employer, bank, credit union, home insurance, or an organization you belong to, like AAA. You can also order free credit reports to help you monitor for fraudulent financial activity in your name.

Who is liable if your identity is stolen?

According to federal regulations, victims have limited liability for debts resulting from identity theft. Generally, you’re not responsible for debts from fraudulent accounts opened in your name. For unauthorized credit card charges, your liability is capped at $50 if reported within 60 days, but some companies waive this entirely. If your ATM or debit card is lost, liability is also limited to $50 if reported within two business days. Most states also have laws limiting liability for fraudulent checks when reported promptly.

* The study was conducted online within the United States by Dynata on behalf of Gen from March 6th to March 2nd, 2024 among 1,003 adults ages 18 and older.

† LifeLock does not monitor all transactions at all businesses.

§ Dark Web Monitoring in LifeLock is not available in all countries. Monitored information varies based on country of residence or choice of plan. It defaults to monitor your email address and begins immediately. Sign into your account to enter more information for monitoring.

Editor’s note: Our articles provide educational information. LifeLock offerings may not cover or protect against every type of crime, fraud, or threat we write about.

This article contains

- What is identity theft insurance?

- How does identity theft insurance work?

- What does identity theft insurance cover?

- Is identity theft insurance worth it? Three questions to ask yourself

- Where can you get identity theft insurance and protection?

- How much does identity theft insurance cost?

- Choose the best option for your situation

- FAQs

Related articles

Identity Theft

What is data privacy? The complete guide

Data privacy is the practice of safeguarding your data. Learn about what data privacy is and why privacy is important for everyone.

September 20, 2024

·

10 min read

Read

More

Identity Theft

Child identity theft: What it is and how to protect your child

Learn how child identity theft occurs and the steps to take to protect your child from it.

June 09, 2025

·

12 min read

Read

More

Scams & Fraud

Tax Fraud: What You Need to Know

Identity thieves and cybercriminals value your identity. They can profit from your personal information by committing identity fraud — to open credit card accounts, obtain loans, and more — all in your name. Learn how to spot and help protect against identity theft.

August 10, 2017

·

3 min read

Read

More

Identity Theft

How to Report Identity Theft to the Credit Bureaus

Identity theft affects millions of Americans every year. Learn how to notify the credit reporting agencies of identity theft and what to expect once you do.

January 02, 2018

·

3 min read

Read

More

Identity Theft

Credit monitoring vs. identity theft protection: What’s the difference?

Do you know the difference between ID theft protection & credit monitoring? Find out now and learn more about which one may be best for you.

March 11, 2024

·

3 min read

Read

More

Identity Theft

How common is identity theft? 24 identity theft statistics

Find out how common identity theft is, areas and ages affected most by identity theft, and other identity theft statistics.

April 08, 2024

·

6 min read

Read

More

Identity Theft

What is data privacy? The complete guide

Data privacy is the practice of safeguarding your data. Learn about what data privacy is and why privacy is important for everyone.

September 20, 2024

·

10 min read

Read

More

Identity Theft

Child identity theft: What it is and how to protect your child

Learn how child identity theft occurs and the steps to take to protect your child from it.

June 09, 2025

·

12 min read

Read

More

Scams & Fraud

Tax Fraud: What You Need to Know

Identity thieves and cybercriminals value your identity. They can profit from your personal information by committing identity fraud — to open credit card accounts, obtain loans, and more — all in your name. Learn how to spot and help protect against identity theft.

August 10, 2017

·

3 min read

Read

More

Identity Theft

How to Report Identity Theft to the Credit Bureaus

Identity theft affects millions of Americans every year. Learn how to notify the credit reporting agencies of identity theft and what to expect once you do.

January 02, 2018

·

3 min read

Read

More

Identity Theft

Credit monitoring vs. identity theft protection: What’s the difference?

Do you know the difference between ID theft protection & credit monitoring? Find out now and learn more about which one may be best for you.

March 11, 2024

·

3 min read

Read

More

Identity Theft

How common is identity theft? 24 identity theft statistics

Find out how common identity theft is, areas and ages affected most by identity theft, and other identity theft statistics.

April 08, 2024

·

6 min read

Read

More

Identity Theft

What is data privacy? The complete guide

Data privacy is the practice of safeguarding your data. Learn about what data privacy is and why privacy is important for everyone.

September 20, 2024

·

10 min read

Read

More

Identity Theft

Child identity theft: What it is and how to protect your child

Learn how child identity theft occurs and the steps to take to protect your child from it.

June 09, 2025

·

12 min read

Read

More

Scams & Fraud

Tax Fraud: What You Need to Know

Identity thieves and cybercriminals value your identity. They can profit from your personal information by committing identity fraud — to open credit card accounts, obtain loans, and more — all in your name. Learn how to spot and help protect against identity theft.

August 10, 2017

·

3 min read

Read

More

Identity Theft

How to Report Identity Theft to the Credit Bureaus

Identity theft affects millions of Americans every year. Learn how to notify the credit reporting agencies of identity theft and what to expect once you do.

January 02, 2018

·

3 min read

Read

More

Start your protection,

enroll in minutes.

Copyright © 2025 Gen Digital Inc. All rights reserved. All trademarks, service marks, and tradenames (collectively, the "Marks") are trademarks or registered trademarks of Gen Digital Inc. or its affiliates ("Gen") or other respective owners that have granted Gen the right to use such Marks. For a list of Gen Marks please see GenDigital.com/trademarks.