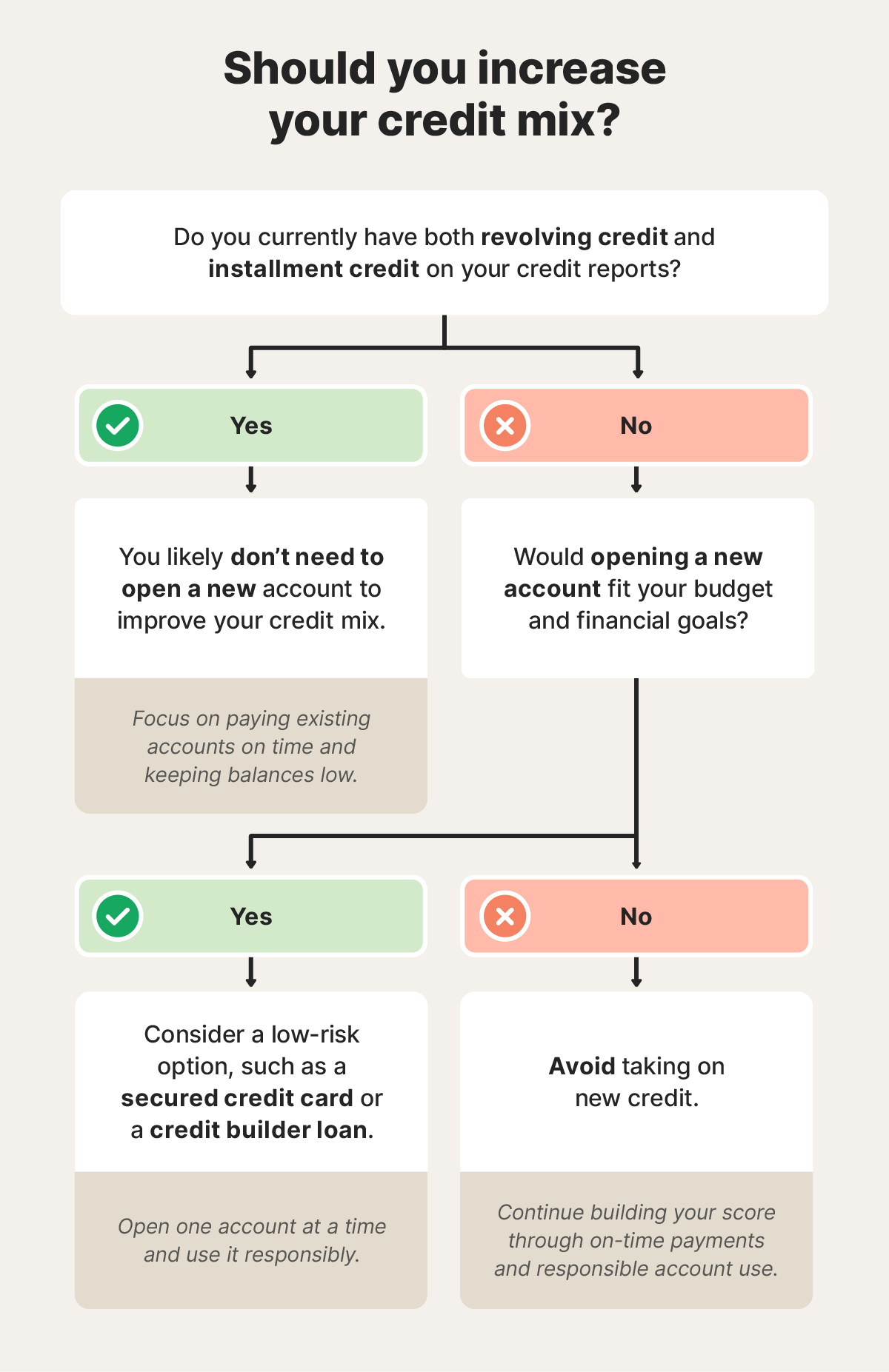

Tip: When looking for ways to improve your credit mix, consider the overall impact on your credit and your financial situation. For instance, opening new accounts can result in excessive hard inquiries and higher balances, which can temporarily hurt your credit score. And, remember to never take on new credit that you can’t afford.

Call us:

1-866-820-4557

Credit mix: What is it, why it matters, and how to improve it

Your credit mix, which is determined by the types of credit accounts you hold, directly impacts your credit score. Read our guide to learn why it matters and how it can help you build stronger credit. Then, get LifeLock to help monitor your credit while you work toward your financial goals.

Credit mix is an important factor in determining your credit, typically making up around 10% of your overall credit score depending on the scoring model used. If you’re one of the 79% of consumers currently trying to improve their credit score, the good news is that it’s possible. By balancing the types of credit you use, you can create a positive impact on your credit score, which demonstrates to lenders that you’re financially responsible.

To help you navigate the confusing terminology and terrain of credit mix, this article will explore what credit mix is, how it affects your credit score, and offer you actionable tips on improving your credit mix.

Why does credit mix matter?

Credit mix matters because it’s one of the five factors used to determine your overall creditworthiness. Having a healthy credit mix, which includes both revolving credit (like a credit card) and installment credit (like an auto loan) shows lenders that you can manage different types of accounts responsibly. For financial institutions, this translates into a lower perceived risk.

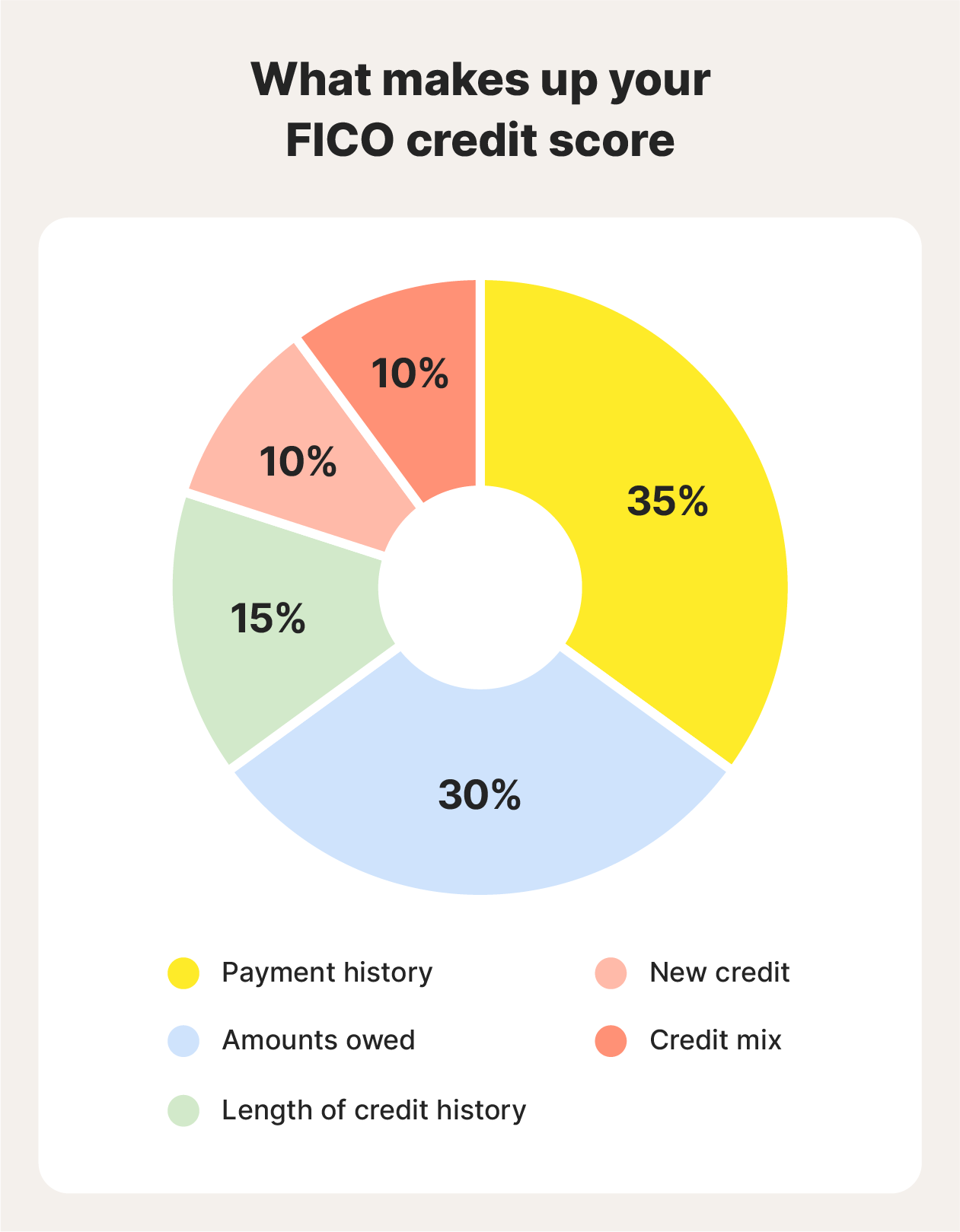

When it comes to your credit score, your credit mix makes up 10% of your FICO score. For VantageScore 3.0, credit mix is part of your depth of credit, which counts for 20-21% of your overall score. While other credit factors, like payment history and utilization, have a bigger impact, having a good credit mix still has the power to improve your credit score.

Between the impact on your credit scores and demonstrating financial responsibility, developing a good credit mix is essential. Plus, it can make you a more attractive borrower.

Pie chart showing what factors make up your FICO credit score.

Types of credit and credit mix examples

There are two main types of credit: revolving and installment. Let’s explore what each type of credit looks like, and review what does and does not affect your credit mix.

Revolving credit

Revolving credit is an open-ended credit line that lets you borrow as needed and repay over time, commonly in the form of a credit card. Unlike loans with a set end date, revolving accounts stay open as long as you remain in good standing. These accounts come with a preset credit limit; for instance, a limit of $2,000 means you can carry a balance up to that amount at any given time.

Each revolving credit account also comes with an interest rate and a minimum payment amount. Here are some types of revolving credit accounts:

- Credit cards: Both unsecured and secured (which require a deposit) credit cards count as revolving lines of credit. Pre-approved credit cards also count as revolving credit.

- Retail store cards: These cards are often promoted at the register and offer discounts and rewards at the specific store, such as the Target Circle card.

- Home equity line of credit (HELOC): Often used to fund home improvements, a HELOC allows you to borrow against the equity you have in your home.

- Personal line of credit (PLOC): Usually reserved for good-credit borrowers, a personal line of credit lets you borrow or withdraw funds as needed.

- Digital line of credit: These accounts allow you to make online purchases using a personalized credit line, such as PayPal Credit.

- Business line of credit: For business owners, when you have an established relationship with a vendor, they may offer you a line of credit for your business purchases.

Installment credit

Installment credit (also known as an installment loan) is a type of credit account in which you borrow a fixed amount of money and repay it over time, such as a mortgage. Repayment terms range from months to years, and interest rates and payment amounts are fixed. For instance, a $20,000 car loan may have a 5-year term, an 8.5% interest rate, and a monthly payment of $410.

By diversifying the types of loans you have appearing on your credit reports, you can strengthen your credit mix and show lenders that you can handle long-term financial commitments. Here are some of the most common types of installment loans:

- Mortgage.

- Auto loan.

- Student loan.

- Personal loan.

- Home equity loan.

- Refinance loan.

There are also loans specifically designed to help you build credit and improve your credit mix, such as credit builder loans (where you don’t actually receive funds until the loan is paid off). Certain buy now, pay later programs may also affect your credit score if the provider reports payments to credit bureaus, but many don’t report on-time payments and only report missed ones.

What isn’t part of a credit mix

Whether a loan or line of credit affects your credit mix depends on the information reported to the credit bureaus. Not all lenders or creditors report accounts to the three major bureaus, especially if the account is temporary. Others report only negative information, such as late or missed payments.

Here are some common types of credit products you may not see appear on your credit reports:

- Payday loans: These high-fee, short-term loans only appear on your credit report if you default. They don’t affect your credit mix.

- Title loans: Secured with your vehicle as collateral, these high-APR (Annual Percentage Rate), short-term loans usually don’t appear on your credit reports unless your account gets sold to collections or your car is repossessed.

- Buy now, pay later loans (BNPL): Many BNPL programs are designed to be short-term and rarely appear on your credit reports. However, certain BNPL accounts may be reported as installment loans (such as Klarna, Affirm, Afterpay) or as revolving accounts (like PayPal credit).

- Rent and utility reporting: In newer scoring models, like FICO Score 9 and 10, reporting rent and utility payments can help you build your credit score. However, these payments are typically treated as payment history rather than a new category of credit.

How to improve your credit mix

To improve your credit mix, you should first assess your financial goals and budget to determine if taking on new debt is worthwhile. If it is, here are some strategies you can use to improve the credit mix portion of your score:

- Add a new type of account: If you only have installment loans reporting, consider opening a revolving credit line. Alternatively, if you only have revolving credit, consider obtaining an installment loan.

- Use a credit builder loan: When you’re starting with very little credit, no credit, or trying to rebuild your credit, a credit builder loan can help you improve aspects of your score, including payment history and credit mix.

- Keep existing accounts open: If you have only one installment loan or revolving credit card, closing it will remove that account type from your credit mix. Keep at least one of each type active to maintain a diverse credit mix — unless they’re costing you financially, for example, with high annual fees.

- Avoid applying for multiple accounts at once: Instead, focus on opening one account at a time and using it to build and improve your credit slowly, but steadily.

Focus on creating a healthy mix of both revolving and installment credit accounts. While a single account can establish credit, a healthy credit mix typically requires more than one type of account over time. And remember, your payment history is the most impactful part of your credit score, so don’t let improving your credit mix get in the way of making timely payments.

A flowchart to help readers determine whether or not they should increase their credit mix.

Keep tabs on your credit with LifeLock

When trying to improve your credit mix, it's essential to regularly monitor your credit reports and credit score. Not only can this help you gauge your credit progress, but it can also alert you to potential problems. With credit monitoring services through LifeLock, you’ll get notified when there are changes to your credit report, which could alert you to fraud.

LifeLock can also help you protect your credit with dark web monitoring, data breach alerts, and privacy monitoring. And if your information is compromised and fraudsters damage your credit, LifeLock can help you get your identity back.

FAQs

Can adding a new account hurt my credit score?

In the short term, adding too many new credit accounts can temporarily hurt your credit score, because each requires a hard inquiry. However, the impact is usually minimal and relatively short-lived. Additionally, a new account can decrease your average age of accounts. The fewer accounts you have, the bigger the impact. But this negative effect decreases over time.

How can I improve my credit mix without opening accounts?

Becoming an authorized user on someone else’s credit card may help if you lack revolving accounts on your credit report. And getting your rent and utility payments reported for free through tools like Experian Boost may help you improve your credit.

How long before a new account improves my credit mix?

Generally, the impact on your credit mix will be reflected as soon as the new account appears on your credit report. Some new accounts, like credit cards, will typically appear on your report in 30 to 60 days.

Editors’ note: Our articles provide educational information about identity theft, scams, financial fraud, and other topics that can put your identity or personal accounts at risk. LifeLock offerings may not cover or protect against every type of crime, fraud, scam, or threat we write about. For more details about how we write, review, and update our articles, see our Editorial Policy.

Related articles

Start your protection,

enroll in minutes.

LifeLock is part of Gen – a global company with a family of trusted brands.

Copyright © 2026 Gen Digital Inc. All rights reserved. Gen trademarks or registered trademarks are property of Gen Digital Inc. or its affiliates. Firefox is a trademark of Mozilla Foundation. Android, Google Chrome, Google Play and the Google Play logo are trademarks of Google, LLC. Mac, iPhone, iPad, Apple and the Apple logo are trademarks of Apple Inc., registered in the U.S. and other countries. App Store is a service mark of Apple Inc. Alexa and all related logos are trademarks of Amazon.com, Inc. or its affiliates. Microsoft and the Window logo are trademarks of Microsoft Corporation in the U.S. and other countries. The Android robot is reproduced or modified from work created and shared by Google and used according to terms described in the Creative Commons 3.0 Attribution License. Other names may be trademarks of their respective owners.