How to spot + avoid student loan forgiveness scams

How to spot and avoid student loan forgiveness scams

Scammers can prey on your financial stress and anxiety. Promises to take some financial weight off your shoulders can be tempting, but some of those offers may be student loan forgiveness scams. Learn the warning signs of student loan scams and how to avoid them. And get an identity protection service like LifeLock that can help you recover stolen funds* in case of identity theft.

If you’re a college student or graduate, it’s essential to be on the lookout for student loan forgiveness scams. With the right knowledge and tools, you can learn to spot and avoid a scam before you become a victim.

Online scams and back-to-school scams can come in many forms, targeting particular groups of people and capitalizing on current events, such as the Biden-Harris Administration’s one-time debt-relief program.

Here are some warning signs of student loan forgiveness scams, including what to do when you come across them:

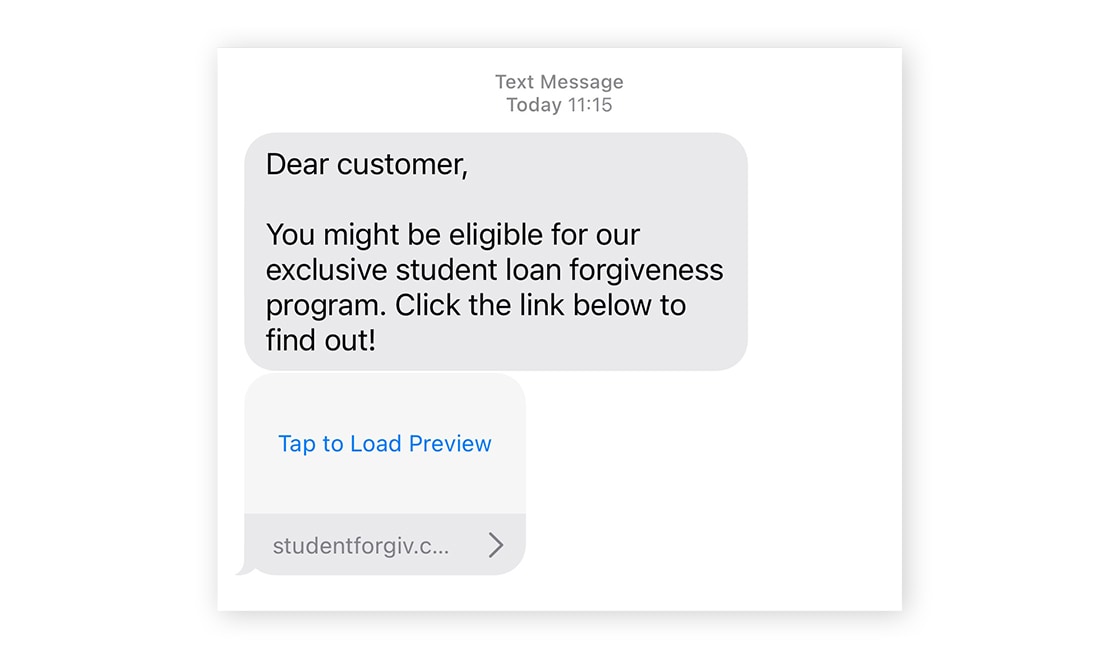

1. Unsolicited communication

Spammy emails, constant phone calls about student loan forgiveness, and text messages from unrecognizable numbers all claiming you might be eligible for a student loan forgiveness program — these annoying tactics are often how student loan forgiveness scams start.

Whether it’s vishing (voice phishing) or smishing (SMS phishing) asking for personal details, this type of unsolicited communication should immediately put you on high alert. Even if the communication includes specific information, such as your current loan balances, don’t be fooled.

Educate yourself so you know what official communication about your student loans really looks like — it could protect you from phishing of all kinds.

Here’s how to react if you receive unsolicited communication about your student loans:

Phone calls: Immediately hang up the phone, then block the caller’s number.

Text messages: Block the sender’s number and delete the message.

Emails: Report the email as spam, then delete the email.

Letters: Throw out the letter or shred it if it contains personally identifiable information such as your Social Security number.

2. Promises that sound too good to be true

The promise of no more student loan debt can be compelling, but like most things that sound too good to be true, this probably is too. The reality is that the majority of borrowers have to pay off their student loans in full, regardless of whether they have a private or federal loan.

And although there are federal programs that can legitimately discharge a portion of your debt, these programs have many qualifying conditions, such as employment in specific fields.

Here’s how to react if an offer of student loan forgiveness sounds too good to be true:

Do your own research to check if what they’re offering is really possible.

Don’t engage with the person or company until you’re certain they’re legitimate.

Ignore the offer and focus on getting yourself in the best position to pay back your student loans, making regular payments, and using federal programs you may qualify for.

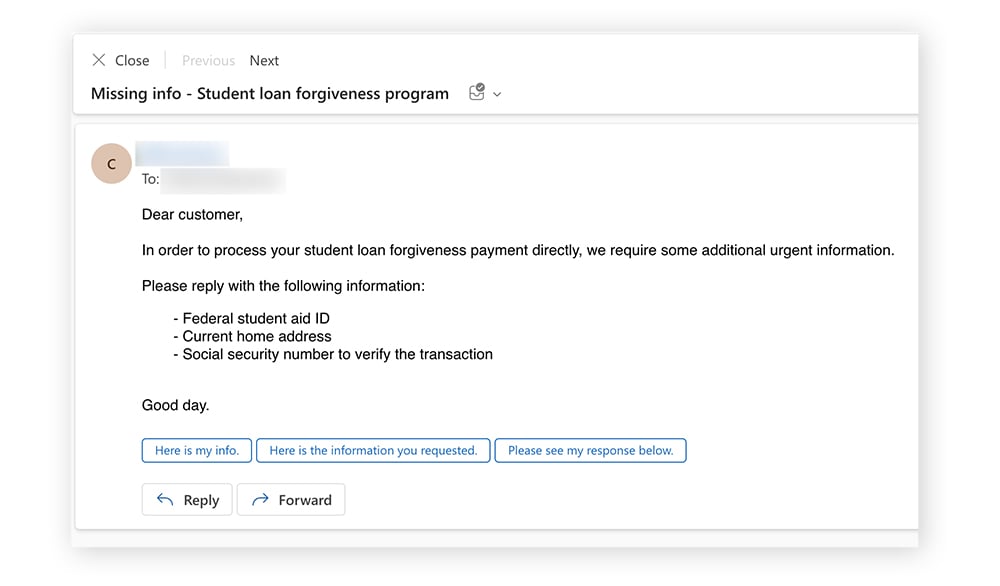

3. Requests for your personal information

If someone asks for your Federal Student Aid ID, it’s a huge red flag. The U.S. Department of Education and your federal student loan servicer (the company that manages the billing for your student loan) will never ask you for your login credentials. Be just as cautious if asked for your date of birth, Social Security number, or other personally identifiable information as giving out these details can lead to identity theft.

Here’s what to do if a student loan forgiveness scammer is asking for your personal information:

Do not give them your FSA ID, account login details, or any other personal information.

Tell them you’ll call them back with the details they’re after. Then do some research to verify the legitimacy of the call.

Put simply, if anyone asks for money upfront to help you apply for student loan forgiveness, it’s a scam. The same goes for fees to consolidate your loans, lower your interest rates, or find scholarships and grants.

The Department of Education and its trusted partners never require payment to assist you with a federal student aid program application. And if someone suggests setting up “monthly maintenance payments” using your credit card, don’t be fooled — this is credit card fraud in action.

Here’s what to do if you’re being asked for an upfront payment:

Don’t make any payments or give the scammer your credit card or bank account details.

Don’t sign contracts or documents committing you to future payments.

Contact your bank and credit card company to place a fraud alert on your account and stop the scammer from making any transactions.

5. A sense of urgency

Creating a sense of urgency is a common tactic scammers use to try and push you into a hasty decision or handing over your credit card details before you have a chance for due diligence. Someone who insists you only have a few days or weeks to apply for their student loan service is likely using social engineering to manipulate you into falling for their scam.

Here are some tips for how you can react in this situation:

Ask for time to do your own research before going ahead with any offer. If the company continues to pressure you to act quickly, it’s likely a scam.

If you have private loans, contact your lender directly to check if the offer is legitimate.

For federal loans, go to studentaid.gov to learn about your real student loan repayment and legitimate forgiveness options.

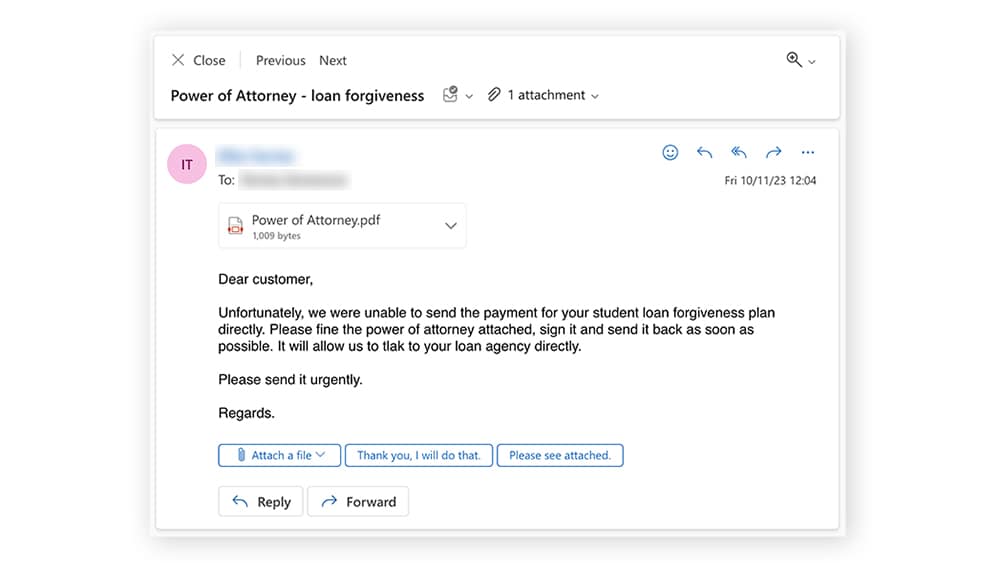

6. Pressure to sign legal documents

Putting pressure on you to sign a legal document is one of the common indicators of a student loan repayment scam. Although a request to sign a power of attorney or third-party authorization form may not be a red flag in itself, if you’re being pressured to sign a document so a person or company can speak to your loan servicer on your behalf, examine it closely and think twice before you sign. The same goes for other legal documents, such as contracts or payment authorizations.

If you’re being pressured to sign legal documents, here’s how you can respond:

Ask for more time to review the documents thoroughly and seek independent legal advice before signing.

Contact your student loan servicer and check the details of the offer with them. They can tell you whether the offer is legitimate and whether you need to sign the documents presented to you.

Decline to sign any documents you are not comfortable with, especially ones that commit you to payments.

7. The caller isn’t associated with the Department of Education

Some private lenders and loan servicers are contracted by the Department of Education to support federal student loans and borrowers. You can check which companies are legitimately associated with the Department of Education by going to the Federal Student Aid website or by phoning the Federal Student Aid Information Center (FSAIC) at 1-800-433-3243. If the company contacting you isn’t a verified loan servicer then it’s highly likely you’re dealing with a scam.

Here are some other ways you can check if the call is legitimate:

Check the URL of the company’s website. If it doesn’t end in [dot]gov then it isn’t affiliated with the federal government.

Google the caller’s phone number to see if it belongs to a legitimate government office.

Know who your student loan servicer is. You can find this out by signing into your FSA account. Your loan servicer information is available on your account dashboard.

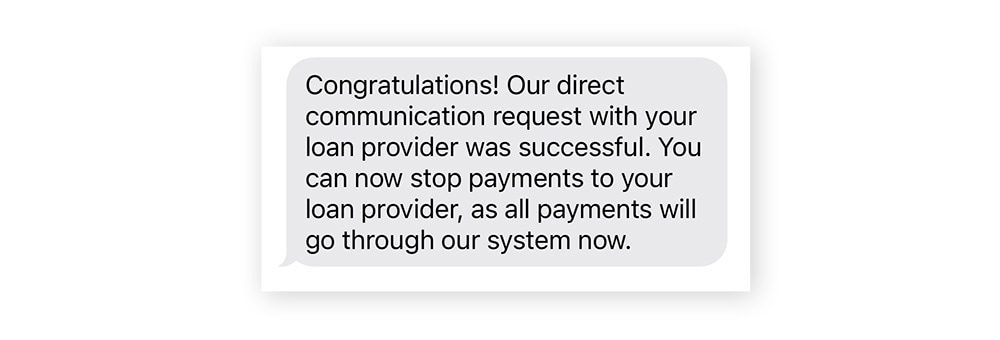

8. Unsolicited advice to halt communication with your loan servicer

Scammers can be very persuasive. They may start with an attractive offer to lure you in, then tell you that since they’ll be working in your best interests, you no longer need to keep in contact with your current loan servicer. If this happens to you, be very cautious. This kind of unsolicited advice should be treated as a major red flag.

If this happens to you, here’s what you can do to avoid the scam:

Don’t give the scammer any information about your student loans.

Don’t stop making payments to your loan servicer unless that servicer tells you to.

Keep in contact with your loan servicer. They can help you sign up for loan forgiveness programs if you’re eligible or change your repayment plan.

Student loan forgiveness scam protection tips

One of the best ways to help protect yourself is to use federal resources or trusted experts to stay informed of student loan forgiveness scams. They say knowledge is power, and that definitely applies here. If you use a keen eye when dealing with loan forgiveness scams, you may be less likely to fall for them.

Here are our top student loan forgiveness scam protection tips:

Avoid suspicious links + attachments: Take a moment to inspect links and attachments before you open them. Whether it's an email or text message, anything that looks odd or is unexpected may be a scam.

Verify information using U.S. government websites: These trusted federal resources are a good place to start:

Reach out to your loan servicer: You can find out who your loan servicer is by signing into your FSA account. Contact them before considering another supposed student loan forgiveness program — it may be a scam.

Know the legitimate options: Here are some of the legitimate student loan forgiveness programs available:

Safeguard your personal information: There are many simple ways you can protect your personal information online. Start implementing best practices today and protect yourself from potential identity theft.

Exercise caution when communicating: Be aware of what information the scammer wants and avoid giving them any additional information about yourself or your loans.

Avoid granting third-party authorization/power of attorney: Stay in control of your own finances by not giving anyone access to your student loan information or authorizing them to act on your behalf.

Take your time: Don’t rush into anything. Give yourself time to fully investigate the options presented to you before making any decisions.

Use identity theft protection services: Using an identity theft protection service like LifeLock can help you protect against scammers by helping you monitor the use of your personal information and notifying you of possible threats to your identity.

What to do if you’re affected by a student loan forgiveness scam

If you know or think you’ve been scammed by a student loan repayment scammer, use trusted federal resources online to mitigate the damage. You should also monitor your payment history, contact your federal loan servicer, and change all passwords to any accounts compromised by the scam.

Follow these recommended actions if you’re affected by a student loan forgiveness scam:

Contact your federal loan servicer: Find out what authorizations are on file and if any unwanted actions have been taken on your loan. Contact details for your loan servicer are available on the Federal Student Aid website.

Contact your bank or credit card company (if affected): Ask them to immediately stop all payments to the company that is scamming you and place a fraud alert on your account to stop scammers from making any transactions.

File a complaint with Studentaid.gov: Report suspicious activity or scams by submitting a complaint on behalf of yourself or someone else.

File a complaint with the Federal Trade Commission: Help fight fraud by reporting the scam to the FTC. They can investigate the scam and use it to educate consumers.

File a complaint with the Consumer Financial Protection Bureau:Reportthe scam to the CFPB so they can investigate the company thoroughly.

Freeze your credit reports: Contact the three major credit bureaus (Equifax, Experian, and TransUnion) to freeze your credit reports to help prevent scammers from opening new accounts in your name.

Change your FSA password: Keep your FSA account secure by signing into Studentaid.gov and changing your password. While you’re there, also check that your account information (email, address, phone number) is accurate. And don’t forget to use a strong password that will be difficult for scammers to guess.

Help avoid student loan forgiveness scams with LifeLock

Avoiding student loan forgiveness scams can be made easier with LifeLock. The Dark Web Monitoring feature scans the dark web and lets you know if your information is found. And it also looks out for potentially fraudulent use of your Social Security number† and other personal info in credit applications.

Dedicated identity restoration specialists are also available to help you if your identity is compromised by a scammer. Put your mind at ease and help avoid fallout from student loan forgiveness scams with LifeLock.

*LifeLock does not monitor all transactions at all businesses.

**Reimbursement and Expense Compensation, each with limits of up to $25,000 for Core, up to $100,000 for Advanced and up to $1 million for Total. And up to $1 million for coverage for lawyers and experts if needed, for all plans. Benefits provided by Master Policy issued by United Specialty Insurance Company, Inc. (State National Insurance Company, Inc. for NY State members). Policy terms, conditions and exclusions at: NortonLifeLock.com/legal

Anna Wratislav is a contributing writer for LifeLock. She specializes in identity protection and how to keep your credit healthy.

Editors’ note: Our articles provide educational information about identity theft, scams, financial fraud, and other topics that can put your identity or personal accounts at risk. LifeLock offerings may not cover or protect against every type of crime, fraud, scam, or threat we write about. For more details about how we write, review, and update our articles, see our Editorial Policy.