1 Based on a 2025 survey conducted by Gen, the company behind LifeLock.

Call us:

1-866-820-4557

Do banks refund scammed money? How to recover your funds

According to Gen research, victims have lost an average of $3,858¹ to scams. And because you can’t always rely on banks to refund scammed money, you may need other solutions to recover your funds.

More broadly, Americans lose an estimated total of $119 billion each year to online scams, according to a 2026 report from the Consumer Federation of America (CFA). And this problem will likely only grow due to AI-powered tools that make modern fraud techniques more convincing and harder to spot than ever.

Whether the loss is $100 or your entire life savings, the impact can be devastating, and victims are often left wondering what their options for recovery are.

While it’s possible to get your money back, many banks only refund scammed money under specific circumstances. Eligibility often depends on how the scam occurred and how quickly you reported it. Let’s dive into how the scam-recovery process works, and how you can help avoid falling victim to scams in the first place.

Do banks refund scammed money?

Sometimes. Whether a bank refunds scammed money depends primarily on Regulation E, the federal law that protects consumers from electronic fund transfer errors. Legally speaking, banks are generally required to refund scammed money if you didn’t authorize the transaction, such as if your account was hacked.

However, if you did authorize the transaction — even under pressure or deception — a refund isn’t guaranteed. Outcomes depend on factors like the payment method, how quickly you report the issue, and your bank’s policies. In many cases, once you hit “send,” the payment is treated as authorized, which can limit your chances of recovery.

As of March 2026, updated Nacha rules offer more protection. Banks are now required to monitor for payments made under false pretenses, including scams involving impersonation of trusted individuals or companies. While refunds still aren’t guaranteed, you may have a stronger case if your bank failed to detect a clear impersonation attempt.

What to do after being scammed

If you suspect somebody scammed you, there are steps you can take to minimize damage and potentially get your money back. Here’s what you should do immediately after being scammed:

- Stop communicating with the scammer: While you might attempt to stay in contact with the scammer to try to get your money back, this approach is unlikely to help you recover the funds. Scammers and cybercriminals make a living out of deceiving people — they won’t respond to guilt, pleas, or even threats of legal action.

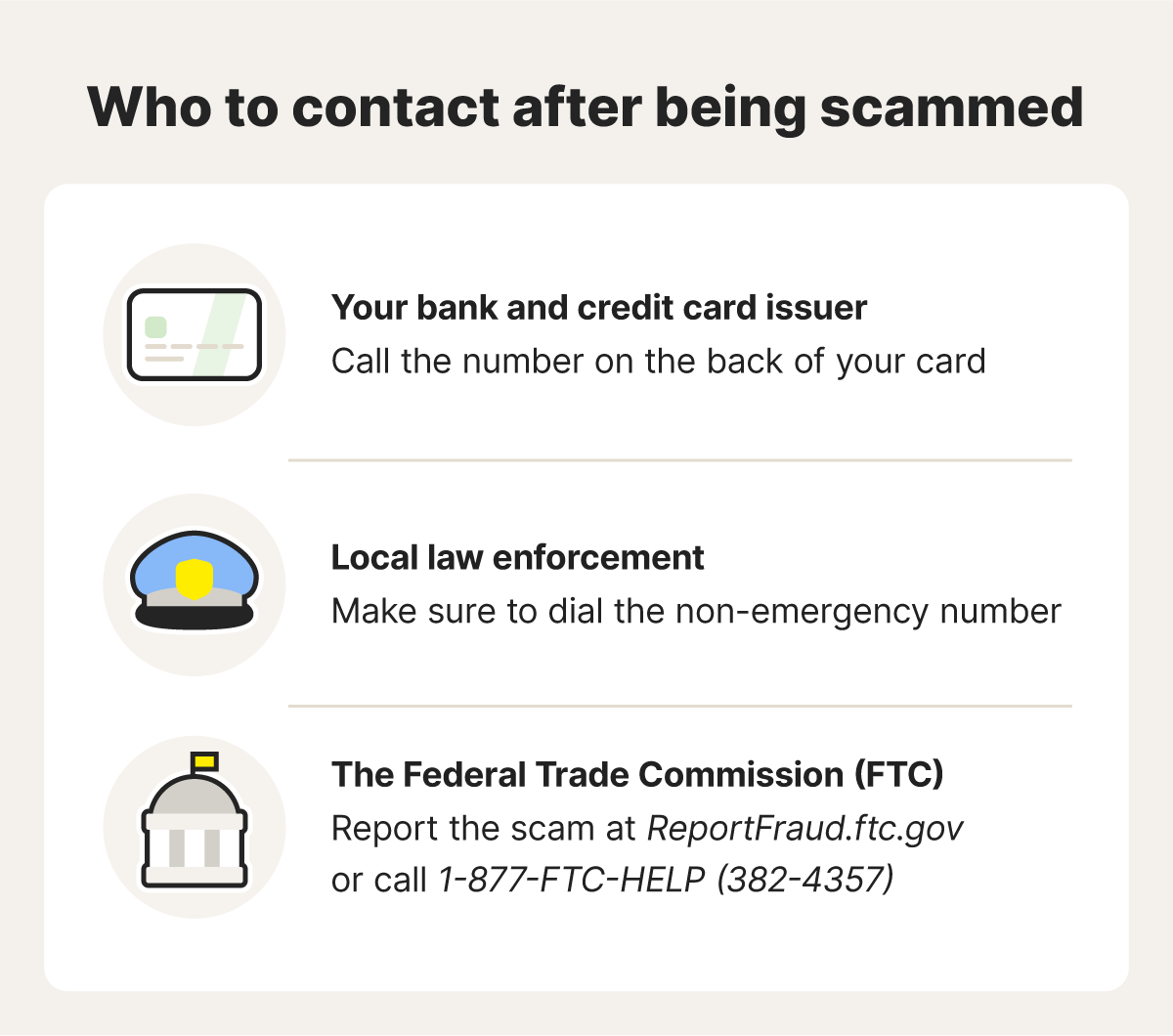

- Notify your bank and credit card issuer: Immediately contact your bank or credit card issuer so they can change your account number, cancel your compromised card, issue you a new one, and potentially refund the charges.

- Protect your credit report: Contact one of the three credit bureaus to place a fraud alert on your credit report, which notifies creditors to verify your identity before extending new credit in your name. Or, place a credit freeze with all three bureaus, which prevents anyone (including you) from opening new lines of credit until it’s lifted.

- Change your passwords: If you provided login credentials or other personally identifiable information (PII) to the scammer, change them immediately. Make sure you create strong passwords for all of your accounts, starting with financial ones.

- Notify the local police: Report the scam to local law enforcement. Getting a police report may help you get refunded later, and reporting a scammer may help other people avoid a scam as well.

- Report the scam to the FTC: You should also file an FTC identity theft report or call 1-877-FTC-HELP.

A graphic showing who to contact after being scammed.

35% of Americans have been targeted by scams,1 so if that includes you, you’re certainly not alone. But why not join a different group, like the millions of customers that already trust LifeLock to protect their identity? With LifeLock, you’ll get reimbursement coverage for up to $10,000 of funds stolen following eligible scams, plus identity theft protection that can help you defend against a scam spiraling into something much worse.

How will a bank refund your scammed money?

If a bank is going to refund your scammed money, they’ll usually do it after reviewing a complaint, but it depends on the scam type and bank policies. Here’s how your bank will likely handle your scam refund depending on your situation:

If you spot an unauthorized transaction

When you report a suspicious charge within the appropriate time frame — usually within 60 days of your bank sending the statement with the unauthorized transaction — your bank conducts an investigation. If the bank finds that you didn’t authorize the transaction, they’ll reimburse you. If you haven’t already canceled the card responsible for the unauthorized charge, do it immediately and request a new card from your bank.

If you paid a scammer

If you have already paid a scammer, your bank might refund you, depending on the payment method, and some methods offer better refund options than others. Of course, if you pay a scammer in cash, there’s little chance a bank will refund you.

Here’s what your bank can do depending on the type of transaction:

- Credit card: These transactions are usually the easiest to refund because the chargeback process is straightforward and well-established. Many credit card companies also provide strong consumer protections.

- Wire transfers: Wire transfers typically aren’t reversible, making it much harder to recover your funds even if you report the scam within the allotted time period.

- Payment apps: Your bank likely won’t return money sent in a payment app, because these apps work as direct transfers between individuals, just like cash or wire transfers. However, some payment apps, like Cash App, may offer their own payment protection plans, so you might be able to get a refund through the app instead.

- Cryptocurrency: This is another payment type that your bank typically can’t reverse, so you’re unlikely to get your money back.

No matter what payment method you use, you should still report the fraud to your bank to see if there’s anything they can do.

If your bank account is compromised

Generally, if somebody hacked your account, your bank will refund your money as long as you report it promptly. However, if you wait too long, your liability increases, and your bank may hold you responsible for all or part of the lost funds. That’s why you should regularly monitor your bank account activity.

How soon can my bank refund scammed money?

Credit card disputes can take up to 90 days to resolve, while banks typically have 10 business days to investigate a fraudulent debit card transaction. However, the bank’s timelines depend on the institution and its investigation process.

Credit card charges

When you dispute a charge with your credit card company, they must verify that they received the dispute within 30 days and complete the investigation within 90 days, according to the Fair Credit Billing Act. If they discover the charge is fraudulent, they’ll credit your account. Some banks may also issue provisional credit to your account while they conduct the investigation.

Debit card charges

Because debit charges have a direct impact on your account balance, banks generally have 10 business days to investigate unauthorized debit card charges. If the bank can’t complete the investigation during this timeframe, they’ll generally issue you temporary credit for the amount of the disputed charge while they continue their investigation.

How to get alternative payments back from a scammer

Banks are less likely to refund scammed money if you used an alternative payment method, such as a wire, cash, a gift card, or a payment app. Some types of insurance may reimburse you after a scam, such as homeowner’s or renter’s insurance, cyber insurance, or business crime insurance.

Depending on the payment type, try the tips below to get a refund for scammed money:

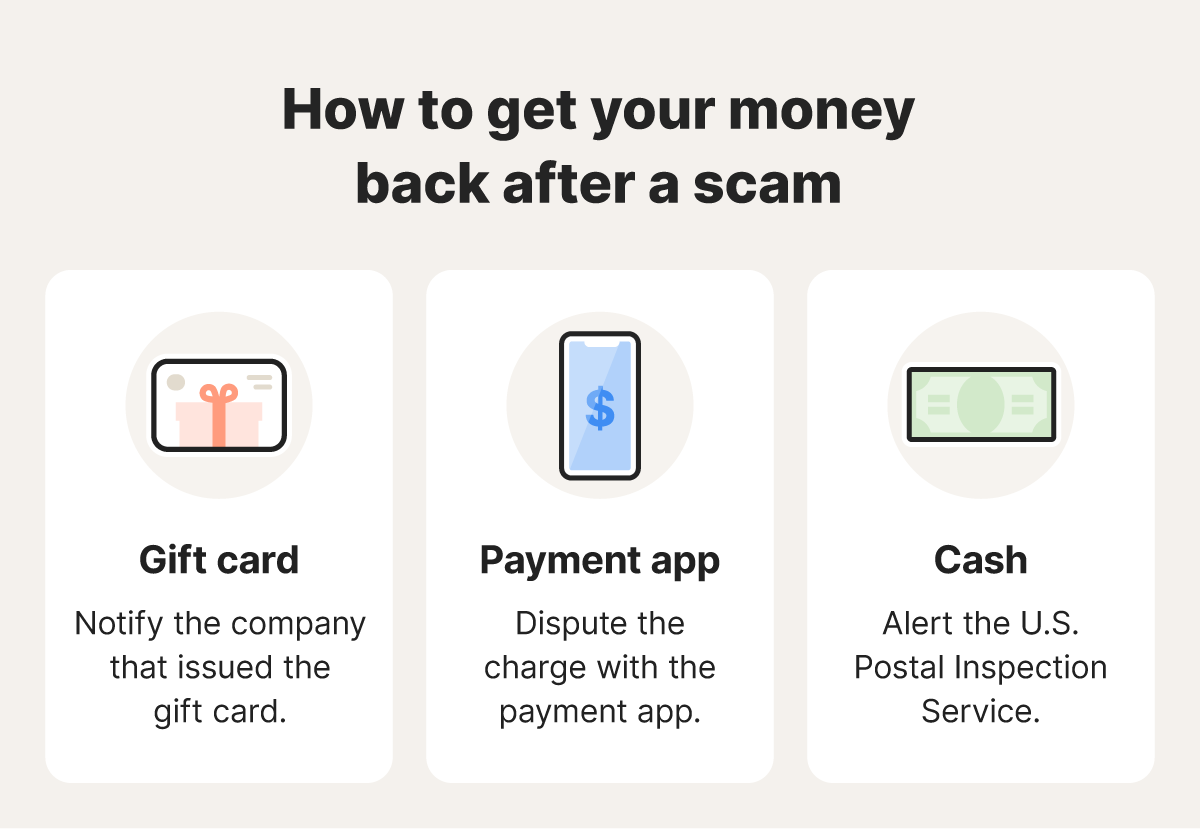

- Contact the gift card issuer: If you unwittingly sent gift cards to a scammer — such as from Amazon, Apple, or Target — you can reach out to the issuer and provide the card information. If the money wasn’t downloaded by the scammer, some companies will refund it.

- Open a dispute with the payment app: If you sent funds to a scammer via a payment app like Venmo, PayPal, or Zelle, you can try to dispute the transaction with the payment app company directly.

- Reach out to the U.S. Postal Inspection Service: If you sent a check or cash by mail to a scammer, contact the U.S. Postal Inspection Service to request that they intercept the delivery.

Graphic showing how to get your money back after a scam depending on the payment type.

How to avoid online scams targeting your bank account

The best way to avoid the headache of trying to get refunded from the bank is to avoid common online scams in the first place. Here are a few tips to help protect your personal information and prevent it from getting into the hands of scammers:

- Never pay over the phone: Don’t send money over the phone for a transaction you didn’t initiate yourself.

- Verify claims: Know that banks and government agencies will never call you for payment or sensitive data over the phone. If you’re unsure, hang up and initiate the contact by yourself through an official channel.

- Don’t click links: Avoid clicking links in emails or texts from unknown senders, as they may be scams or contain malware.

- Secure your accounts: Use strong passwords and enable two-factor authentication (2FA).

- Use security software: Install a tool that blocks fake websites and flags phishing links before you click them.

- Protect your connection: Don’t make financial transactions over public Wi-Fi unless you’re using a VPN to encrypt your connection.

- Trust your gut: Always walk away if something seems suspicious or too good to be true.

Get reimbursed for scam losses with LifeLock

Jumping through hoops to get your money back from a scammer who’s stolen your details can be an arduous task. But LifeLock can help, with scam restoration experts available to help with your recovery and up to $10,000 in reimbursement coverage for scam-related losses. Plus, as a LifeLock member, you’ll also be able to detect potential identity theft risks following a scam with three-bureau credit monitoring and identity alerts.

Editors’ note: Our articles provide educational information about identity theft, scams, financial fraud, and other topics that can put your identity or personal accounts at risk. LifeLock offerings may not cover or protect against every type of crime, fraud, scam, or threat we write about. For more details about how we write, review, and update our articles, see our Editorial Policy.

This article contains

Related articles

Scams & Fraud

Clone cards: Definition, examples, and how to stay safe

November 04, 2025

·

8 min read

Scams & Fraud

What is a brushing scam? Why free packages raise red flags

November 13, 2025

·

10 min read

Scams & Fraud

Clone cards: Definition, examples, and how to stay safe

November 04, 2025

·

8 min read

Scams & Fraud

What is a brushing scam? Why free packages raise red flags

November 13, 2025

·

10 min read

Scams & Fraud

Clone cards: Definition, examples, and how to stay safe

November 04, 2025

·

8 min read

Scams & Fraud

What is a brushing scam? Why free packages raise red flags

November 13, 2025

·

10 min read

Start your protection,

enroll in minutes.

LifeLock is part of Gen – a global company with a family of trusted brands.

Copyright © 2026 Gen Digital Inc. All rights reserved. Gen trademarks or registered trademarks are property of Gen Digital Inc. or its affiliates. Firefox is a trademark of Mozilla Foundation. Android, Google Chrome, Google Play and the Google Play logo are trademarks of Google, LLC. Mac, iPhone, iPad, Apple and the Apple logo are trademarks of Apple Inc., registered in the U.S. and other countries. App Store is a service mark of Apple Inc. Alexa and all related logos are trademarks of Amazon.com, Inc. or its affiliates. Microsoft and the Window logo are trademarks of Microsoft Corporation in the U.S. and other countries. The Android robot is reproduced or modified from work created and shared by Google and used according to terms described in the Creative Commons 3.0 Attribution License. Other names may be trademarks of their respective owners.