What is a CVV number and where to find it

A CVV number is a 3- or 4-digit code printed on a credit or debit card that offers additional proof that you’re the rightful owner of that card. Learn how CVV numbers offer an additional layer of security when shopping online. And get LifeLock for powerful identity theft and stolen wallet protection to help safeguard your digital life.

What CVV stands for and how it works

CVV stands for Card Verification Value. The CVV is a uniquely assigned number that provides retailers with extra proof that it’s actually you using your card and not someone who’s stolen your information.

When you order items online or by phone, the retailers behind these transactions will ask for the name on your card, your credit or debit card’s number, its expiration date, and also for that CVV number.

Your CVV number won’t protect you if you lose your card or someone stole it from you. That person can easily find the CVV number on the back of your card and use it when making purchases in your name. Because of that, it isn’t a good idea to share your CVV. Even though it is not the same as your PIN, safeguard it as such.

But if someone has accessed your credit card or debit card information online and is trying to make a purchase, retailers won’t allow those purchases to go through if they don’t also have your card’s CVV number.

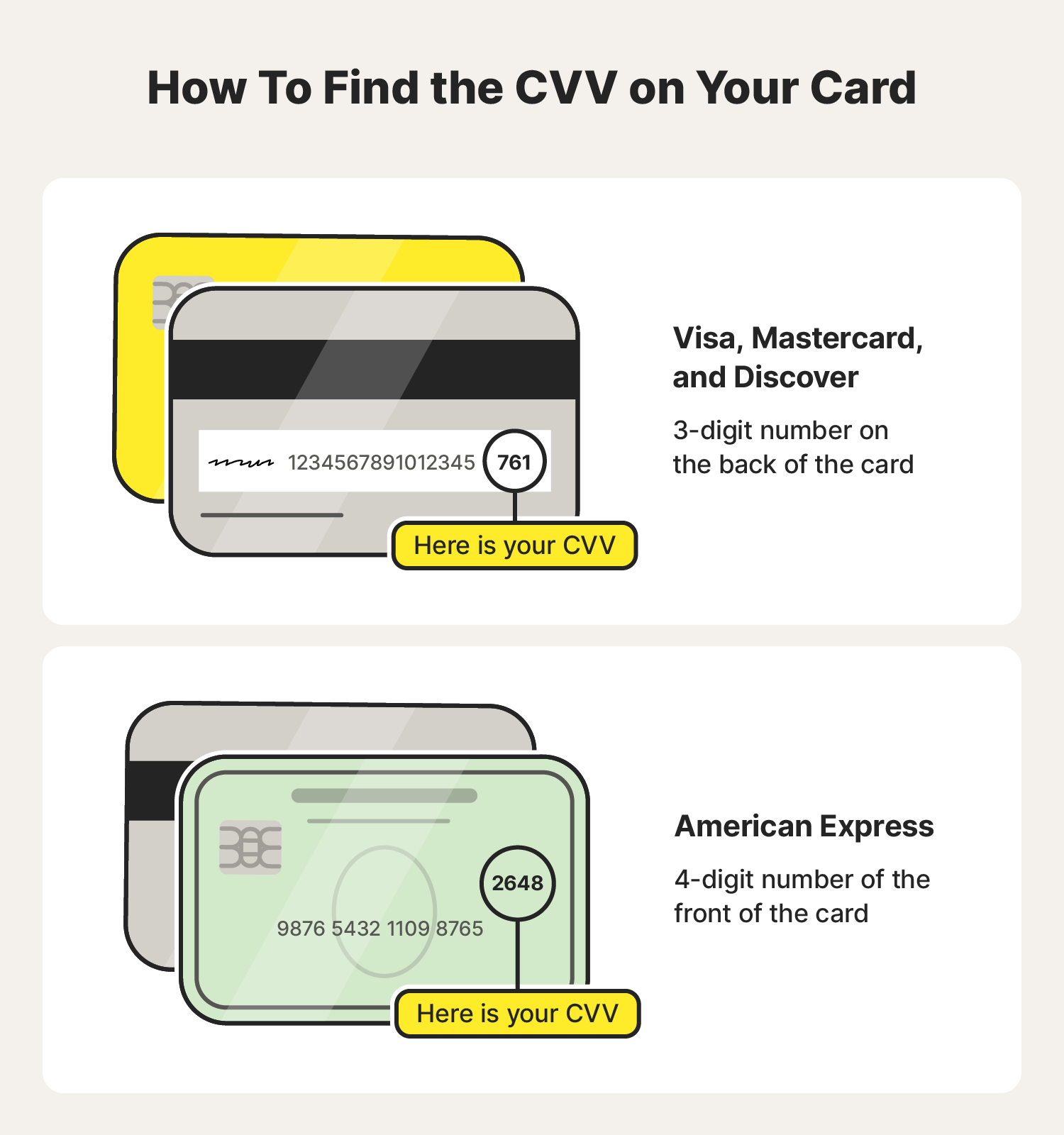

For all Visa, Mastercard, and Discover credit and debit cards, the CVV number is three digits. The CVV code on American Express cards is four digits.

How to find a CVV on a credit card or debit card

You can typically find your CVV on the back of your credit card in the signature area (though it will be on the front if you’re looking at your American Express card).

It’s easy to find your CVV code. If you use credit or debit cards branded by Mastercard, Visa, or Discover, your CVV number will be listed on the back of your credit or debit cards at the end of your card’s signature strip. The location of your CVV number is different if you are using an American Express card. On these cards, a four-digit CVV number will be on the front, right above your card account number.

Other security codes on cards

Credit card companies use different acronyms to refer to their security codes. Here are some of the most common:

| Visa | CVV2 (card verification value) |

| Mastercard | CVC2 (card validation code) |

| Discover | CID (Card ID) |

| American Express and debit cards | CSC (card security code) |

When you use your credit card for online shopping, during the checkout process you will be asked for a CVV even if you are using a Mastercard, Amex, or Discover card. That’s okay—just use whichever code your card has.

How to protect your CVV and credit card

Identity theft can happen to anyone and your CVV, CID, or CVC numbers can’t protect you if you allow them to fall into the wrong hands. Here are some tips for keeping these key four- or three-digit codes safe from thieves.

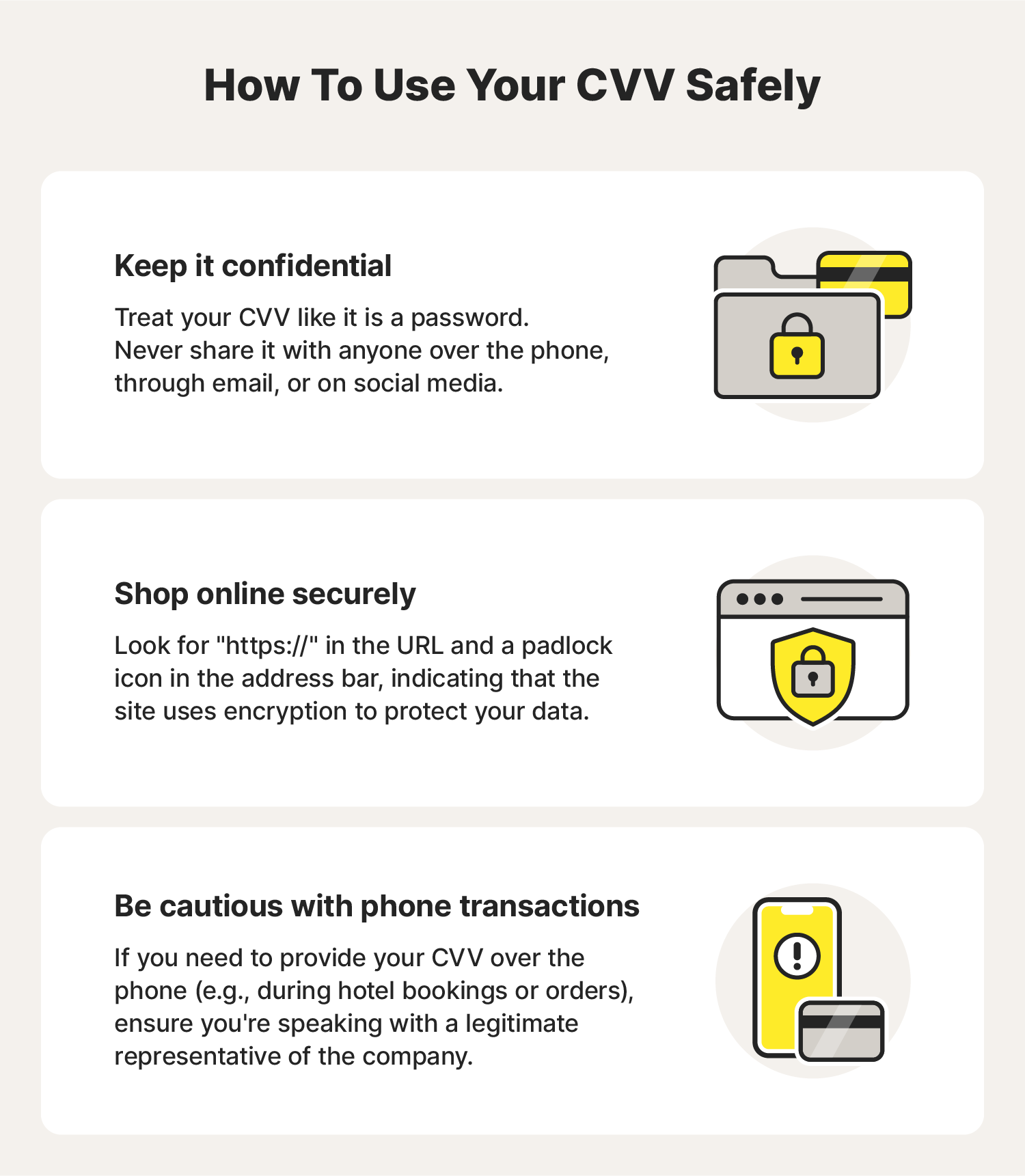

- Never give your CVV number to someone who calls you, even if that person claims to be working with your credit card provider. Credit card companies won’t call you and ask for this information. If someone does, it’s a scammer. Hang up.

- Don’t fall for email phishing attempts. Never provide your credit or debit card information, including your CVV code, to people who ask for it through emails. Scammers often send phishing emails to victims asking that they verify their credit card information to prevent shutdowns of their accounts. This, too, is a scam. Banks will never contact you online to ask for this information.

- Don’t send your credit card or debit card information in an email. Sophisticated cybercriminals can scan your emails, looking for credit card numbers. Never email your credit or debit card numbers or CVV codes to anyone.

- Reduce the number of transactions you make with your debit card. It’s always safer to use credit cards to make online and phone-based transactions. It’s actually safer to use your credit cards for all transactions, including those you make in person, because the fraud protection offered by credit card companies is better than what is offered by your bank. Because credit cards aren’t connected to your money directly, if someone uses your credit, it leaves the money you need to pay bills untouched.

- Don’t save payment information on websites. While it might be convenient, if someone hacks your account, they then have access to your credit card information.

- Don’t give your CVV number to an in-person retailer. When you make a purchase in a store, you don’t need to give the cashier your CVV number. If they ask for it, they could use that information to make online purchases using your card.

Now that you better understand how these CVV codes can help protect your identity, it might be a good time to consider checking that you’re doing everything you can to prevent identity theft. Even small steps—like using a credit freeze or removing personal information from the internet—can have a positive impact.

Protect your financial information

If you really want to make sure your identity is kept safer, sign up for LifeLock. LifeLock membership includes a variety of features to help protect against identity theft, including Dark Web Monitoring to notify you if your personal information leaks and Stolen Wallet Protection to assist you if your wallet is ever stolen.

FAQs about what is a CVV?

Need more answers to your questions about CVVs? We’re here to help!

Where is the CVV on Amex?

The four-digit CVV on an American Express card is printed on the front of the card, over the right side of the account number.

How are CVVs assigned?

The security codes on credit cards aren’t as random as they seem. While the algorithms that the card issuers use to determine a debit or credit card CVV are a well-guarded secret, they use information related to the account, including:

- The primary account number

- The card’s expiration date

- Two standard data-encryption keys

- A service code

What is a dynamic CVV?

A dynamic CVV is a CVV that changes regularly (usually every hour or so). These CVVs are more secure because even if a thief got their hands on your credit card information, the shifting CVVs would severely limit the time they would have to use the card. Some dynamic CVVs are displayed on a mini-screen on the back of the card, and others are sent to you via text message or an app.

Will my new card have a new CVV?

Yes. All new cards, even with the same credit card number, will have a new CVV. This is an extra protective measure the card issuer takes to help reduce credit card fraud.

Does a CVV have 3 or 4 digits?

It depends on which credit card company issued the card. Mastercard, Visa, and Discover all have 3-digit CVVs, while American Express has a 4-digit CVV.

What’s the difference between a CVV and CVV2?

CVV and CVV2 numbers are card security codes. The “2” in CVV2 is because the number was generated using a second-generation process to make it less likely to be guessed.

Is it safe for me to share my CVV?

No, it isn’t safe to share your CVV with anyone. It is safe to use it when you shop online because the processing is encrypted and the retailer never sees your CVV. But if you share your CVV number with someone in person or over the phone, it could be the last piece of the puzzle they need to start making charges on your card.

Is my CVV the same as my PIN?

No, it isn’t. A PIN—Personal Identification Number—is a four-digit code cardholders use when making purchases or using ATMs with their debit cards. They might also use a PIN when using their credit cards to complete a cash advance at an ATM. Keeping your PIN and CVV numbers safe is a big part of protecting yourself from identity theft.

Editors’ note: Our articles provide educational information about identity theft, scams, financial fraud, and other topics that can put your identity or personal accounts at risk. LifeLock offerings may not cover or protect against every type of crime, fraud, scam, or threat we write about. For more details about how we write, review, and update our articles, see our Editorial Policy.

Related articles

Start your protection,

enroll in minutes.

LifeLock is part of Gen – a global company with a family of trusted brands.

Copyright © 2026 Gen Digital Inc. All rights reserved. Gen trademarks or registered trademarks are property of Gen Digital Inc. or its affiliates. Firefox is a trademark of Mozilla Foundation. Android, Google Chrome, Google Play and the Google Play logo are trademarks of Google, LLC. Mac, iPhone, iPad, Apple and the Apple logo are trademarks of Apple Inc., registered in the U.S. and other countries. App Store is a service mark of Apple Inc. Alexa and all related logos are trademarks of Amazon.com, Inc. or its affiliates. Microsoft and the Window logo are trademarks of Microsoft Corporation in the U.S. and other countries. The Android robot is reproduced or modified from work created and shared by Google and used according to terms described in the Creative Commons 3.0 Attribution License. Other names may be trademarks of their respective owners.