While credit lock vs. freeze might sound different, they function similarly: A credit freeze is a free service that stops new accounts from being opened, while a credit lock is a service from the credit bureaus that lets you lock and unlock your credit faster than a freeze. Both options can help when you’re worried that someone has stolen your identity and may try to open credit accounts under your name.

With identity theft protection, like the kind you get with LifeLock Standard, you can help reduce the damage done by identity theft from those who may try to run up thousands of dollars of debt or damage your financial security.

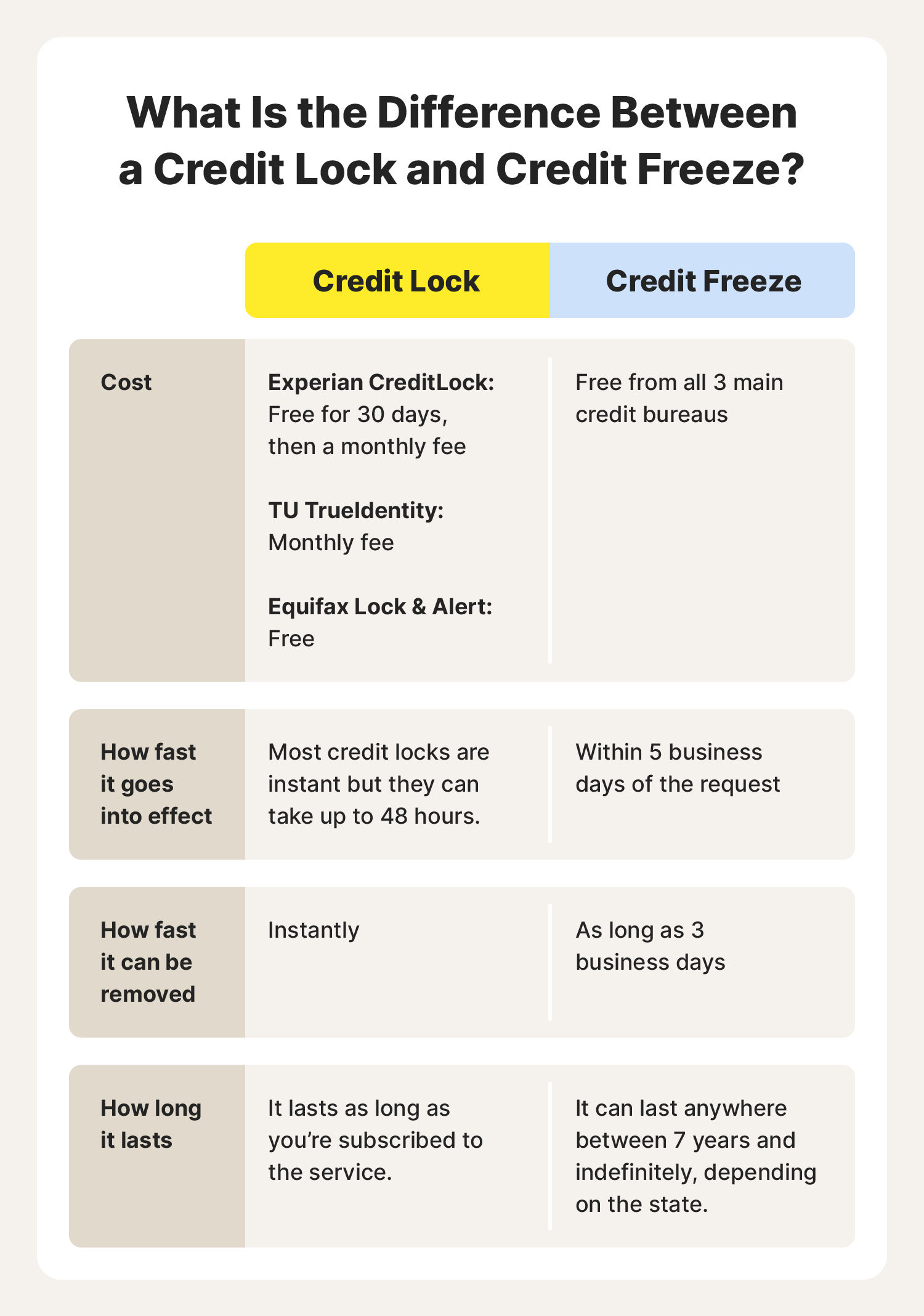

What is a credit freeze?

A credit freeze is a federally regulated temporary restriction that you can place on your credit report. When there is a freeze on your credit report, no one (not even you) can open a new credit account. A freeze is a good idea if you are trying to safeguard your credit after your identity was stolen or if you want to reduce the likelihood of someone trying to use your name to open fraudulent accounts.

Credit freezes are free and can be temporarily lifted (perfect for when you want to apply for a new credit card, auto loan, or mortgage) whenever you want. Depending on where you live, a freeze may be indefinite, or it may have an upward limit on how long it lasts if you don’t request removal.

Because you can remove the freeze when needed, putting a freeze on your report can give you some peace of mind that you wouldn’t have if your report isn’t frozen.

How to freeze your credit

The process for freezing your credit is pretty simple. You’ll need to have some basic information on-hand, including:

- Your name (or your child’s name if you’re freezing their report)

- Address

- DOB

- Social Security number

- Driver’s license or passport

Then you’ll contact each of the three main credit bureaus by phone or using their website:

- Equifax: 1-800-349-9660 or visit Equifax credit freeze.

- Experian: 1-888-397-3742 or visit Experian credit freeze.

- TransUnion: 1-800-680-7289 or visit TransUnion credit freeze.

During the process of freezing your credit, you’ll create a PIN to use when you want to lift or remove the freeze.

Advantages and disadvantages of a credit freeze

| Advantages | Disadvantages |

| Free | Freezes take longer to go into effect compared to locks |

| May last indefinitely | Unfreezing takes longer than credit unlocking |

| Can be lifted temporarily or removed at will | May have a limited length of protection |

| Prevents identity thieves from applying for new credit accounts |

Protecting your credit with a freeze doesn’t have many disadvantages. Compared to a credit lock, it can take a little longer to freeze or unfreeze your credit report (which can feel a lot longer if your identity has been compromised), but you can’t beat the cost, and it’s nice to know that the freeze won’t be canceled just because you don’t want to pay for extra services.

What is a credit lock?

A credit lock is a faster credit freeze service provided directly by the main credit bureaus. With a credit lock service, you can instantly lock and unlock your credit, sometimes by using an app on your smart device. Some credit bureaus offer credit locks as one service in a bundle of products designed to improve your creditworthiness or protect your identity.

You don’t need to lock and freeze your credit report—one or the other at each credit reporting agency is good.

How to lock your credit

To lock your credit, you have to sign up (and pay) for the services with each credit bureau.

- Experian: The Experian credit lock service is CreditWorks Premium, a paid suite of products featuring credit lock and identity theft protection.

- TransUnion: You can enroll in TranUnion’s Credit Monitoring service and pay a monthly fee.

- Equifax: Credit Lock & Alert is a free service for locking your Equifax report.

For the paid services, if you stop subscribing, any locks you have activated will be turned off, so make sure you’re prepared to freeze your credit if you want the protection without the price tag.

Advantages and disadvantages of a credit lock

| Advantages | Disadvantages |

| Credit is locked more quickly than a freeze | It costs money to use a credit lock |

| Credit can be unlocked almost instantly | Most credit bureaus charge separately for credit lock services |

| Can be bundled with other services | Might be attached to services you don’t need |

| Prevents identity thieves from applying for new credit accounts | Only lasts until you cancel the service |

Credit locks might be worth the cost for you and your family if you’ve had your identity stolen or you need to be able to quickly lock and unlock your report. If credit locking is bundled with other services like credit monitoring or identity theft detection, it could be worth the cost, but remember that locking your credit with all three agencies could mean paying multiple fees.

When should you freeze or lock your credit?

You should freeze your credit if you think you’ve been the victim of identity theft or if your financial or personal information has been exposed to a data breach. But these aren’t the only times you should consider a credit freeze. If you want more consistent protection from identity theft, you should keep your credit frozen unless you actively apply for a new loan or credit card. When you apply for new credit or debt, you can temporarily unfreeze your credit.

Make sure that you freeze your credit at all three credit bureaus. Freezing or locking at only one bureau will leave you unprotected with the others.

Help protect your credit

Now that you have a better understanding of a credit lock vs. freeze, it might be time to examine your credit report to look for any errors or fraud. If you find anything suspicious, report it to the credit reporting agencies immediately, then consider investing in identity theft protection with LifeLock Standard.

LifeLock Standard monitors the dark web for your information, helps you replace or cancel credit cards, IDs, and other important documents if you lose your wallet as a result of identity theft, and will assign you a dedicated Identity Restoration Specialist to help you if your identity is stolen.

FAQs about credit lock vs. freeze

Have more questions about a credit freeze vs. lock? We have answers.

Does a credit freeze prevent soft inquiries?

Because a soft inquiry is not necessarily to open a new credit account, a credit freeze usually doesn’t prevent soft inquiries. Certain companies (insurance providers, for example) can still look at your credit report, as can your existing creditors.

What happens when you freeze your credit?

When you freeze your credit, new credit accounts cannot be opened under your name.

What is a fraud alert?

A fraud alert is a warning placed on your credit report that advises creditors to take extra steps to confirm the identity of a person applying for credit. It’s less formal than a lock or freeze, but it provides additional protection against an identity thief trying to apply for new credit.

How long does a credit freeze last?

It depends on your state. Some states have laws requiring credit bureaus to freeze your credit indefinitely, while others cap the length of a freeze.

Will a credit freeze affect your credit score?

Freezing your credit will not affect your credit score, but your credit score can still change during a freeze based on the normal factors that affect your score.